Banking & Finance

Sustainable Finance – Are you ready for 10 March 2021?

Author: Kurt Hyzler

Author: Kurt Hyzler

Sustainable finance has, after years of ongoing debate, finally come to the forefront of regulation within the EU. Until now, financial regulation has primarily required financial institutions to focus on financial risks for clients. Increasingly, there is a demand that such institutions look at investments’ sustainability risks and opportunities. Sustainability factors include inter alia climate change, environmental, social and employee issues, respect for human rights, and anti-corruption and anti-bribery matters.

The EU regulation on sustainability-related disclosures in the financial services sector (the “SFDR”) introduces various disclosure-related requirements for financial market participants and financial advisers at the entity, service and product level with regards to:

- The integration of sustainability risks into business practices;

- The consideration of adverse sustainability impacts in their processes; and

- The provision of sustainability-related information with respect to financial products.

The spirit of the SFDR is to enable EU based investors to make informed decisions regarding Environmental, Social and Governance (“ESG”) considerations for their investment decisions. The SFDR works alongside the EU’s Taxonomy Regulation and its objectives to identify those economic activities which are considered environmentally sustainable. The majority of the SFDR obligations will be applicable as of 10 March 2021. Firms falling in scope will need to ensure they have all the relevant disclosures and policies in place which may present certain challenges given this tight deadline.

WHO FALLS IN SCOPE?

The SFDR has implications for investment services licence holders defined in the SFDR as Financial Market Participants, Financial Advisers, and Financial Products, with disclosure requirements applying both at “entity” level and at “product” level.

Entity-level:

Financial Market Participants include investment services licence holders such as UCITS Management Companies, alternative investment fund managers (“AIFMs”), MiFID firms which act as portfolio managers of locally based Professional Investor Fund (“PIF”) structures by way of delegation.

Financial Market Advisers include EU investment services licence holders which provide investment advice.

Product-level:

Financial Products include all investment services licence holders such as UCITS, AIFs and MiFID portfolios or segregated accounts marketed in the EU.

DISCLOSURES

Websites

At entity level, firms will be required to update their websites with information on the firm’s policies on the integration of sustainability risks into the investment decision-making process/investment advisory process when it comes to investment decisions or advice. Remuneration policies will also need to be updated accordingly to ensure they are consistent with the aforementioned sustainability risk policies, and this information should also be disclosed on the firm’s website.

Principle Adverse Impact (“PAI”) on Sustainability Factors

The PAI is the adverse sustainability impact which will take into consideration any negative, material or likely to be material consequences on sustainability factors that are caused, intensified by or directly linked to investment decisions/advice performed by the firm in question. Disclosures will need to be made on the firm’s website, and in any of the pre-contractual documentation of the products, taking a “comply or explain” approach, whether PAIs on sustainability factors are considered, and if not, a statement on non-considerations with reasons why explained. For large entities with over 500 employees and parent companies of such large groups, the PAI disclosure is mandatory, and such entities need to start considering the PAI by 30 June 2021 at the latest.

Pre-contractual disclosures

To fulfill the product disclosure requirements, financial entities need to classify the products they manage or advise into three categories: products with no focus on sustainability (“Mainstream Products”); products that promote environmental or social characteristics (“Article 8 Products”); and products with sustainability or a reduction in carbon emissions as their investment objective (“Article 9 Products”). For all three categories a “comply or explain” approach will need to be taken within the products’ pre-contractual documentation, such as the offering memorandum. If sustainability risk is deemed to be relevant, the disclosure must outline how sustainability risks are integrated into the investment decision/advice and the results of the assessment of the likely impacts of sustainability risk on their financial return. Where sustainability risk is deemed not to be relevant, a statement to that effect must be disclosed, together with an explanation of the reasons why.

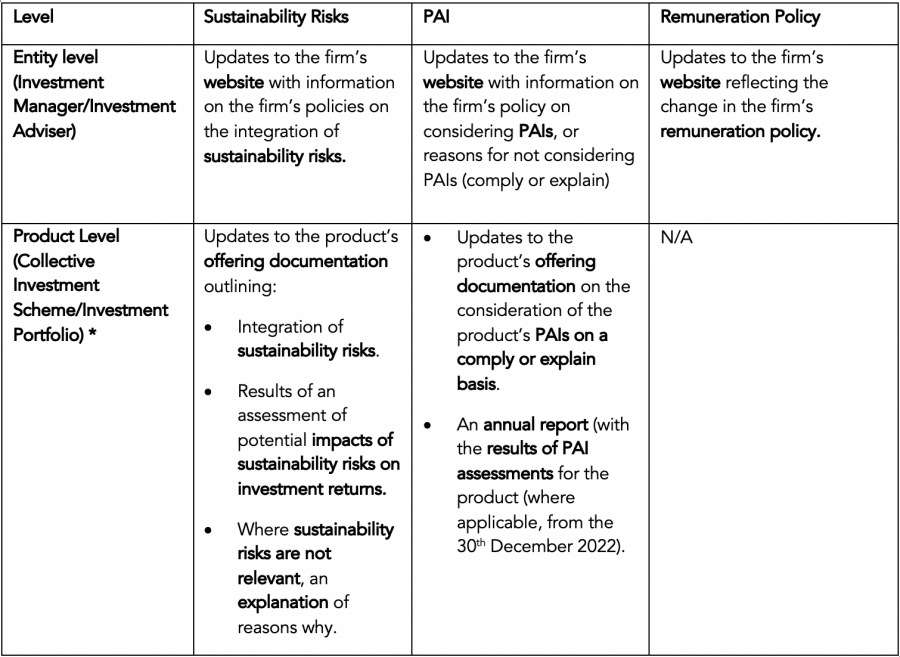

A summary of disclosure obligations for fund managers and funds under the SFDR is depicted in the following table:

Article 8 & 9 Products:

For Article 8 Products and Article 9 Products, further disclosures on the products’ websites and within pre-contractual documentation are to be made including inter alia, providing information on how the environmental or social characteristics are met or, how the sustainable investment objectives are to be attained. As from 1 January 2022, such products must also include disclosures in their periodic reports.

Although categorising Financial Products into Article 8 and 9 Products will add time-consuming assessments on underlying investments and burdensome reporting requirements, especially since certain environmental and social information may not be very accessible, firms who opt to classify and promote their products as Mainstream Products may also be negatively impacted, as the demand for sustainability by investors increases. The same applies for firms opting for the “explain” rather than the “comply” approach for the integration of sustainability risk and the PAI on sustainability factors. Worldwide, there is a demonstrated growing awareness among companies, investors, and shareholders alike that to remain viable, businesses must think about and manage their impact on sustainability in new ways.

Draft RTS

On 4 February 2021, the Joint Committee of the three European Supervisory Authorities (EBA, EIOPA and ESMA – ESAs) delivered to the European Commission (EC) the Final Report which includes the draft Regulatory Technical Standards (RTS), on the content, methodologies and presentation of disclosures under the EU Regulation on the SFDR. Although not yet endorsed by the EC, the RTS will give a good indication on what is expected from financial entities and products on the required disclosures and considerations to be made in light of the SFDR.

Upcoming amendments to the AIFM directive, UCITS directive and MiFID are also expected to incorporate ESG elements.

MFSA CIRCULAR

On 9 February 2021, the MFSA issued a Circular on the local implementation of SFDR and the process which it will adopt for the submission of updates made to the offering documentation of licensed Collective Investment Schemes (“CISs”). The MFSA has established a fast-track filing process whereby UCITS management companies, AIFMs and MiFID investment firms will be able to “self-certify” their compliance with SFDR and notify the MFSA accordingly. The circular also lists the documentation to be filed with the MFSA and emphasises that submissions are to be made by the 10 March 2021. It is also advised that any submissions made after 3 March 2021 will be processed on a ‘best-efforts’ basis by the MFSA.

If you require any further information and/or assistance regarding the SFDR, the required MFSA filings and updates to the pre-contractual documentation of locally licensed CISs kindly contact us on finance@gvzh.mt.